Carmignac's Note

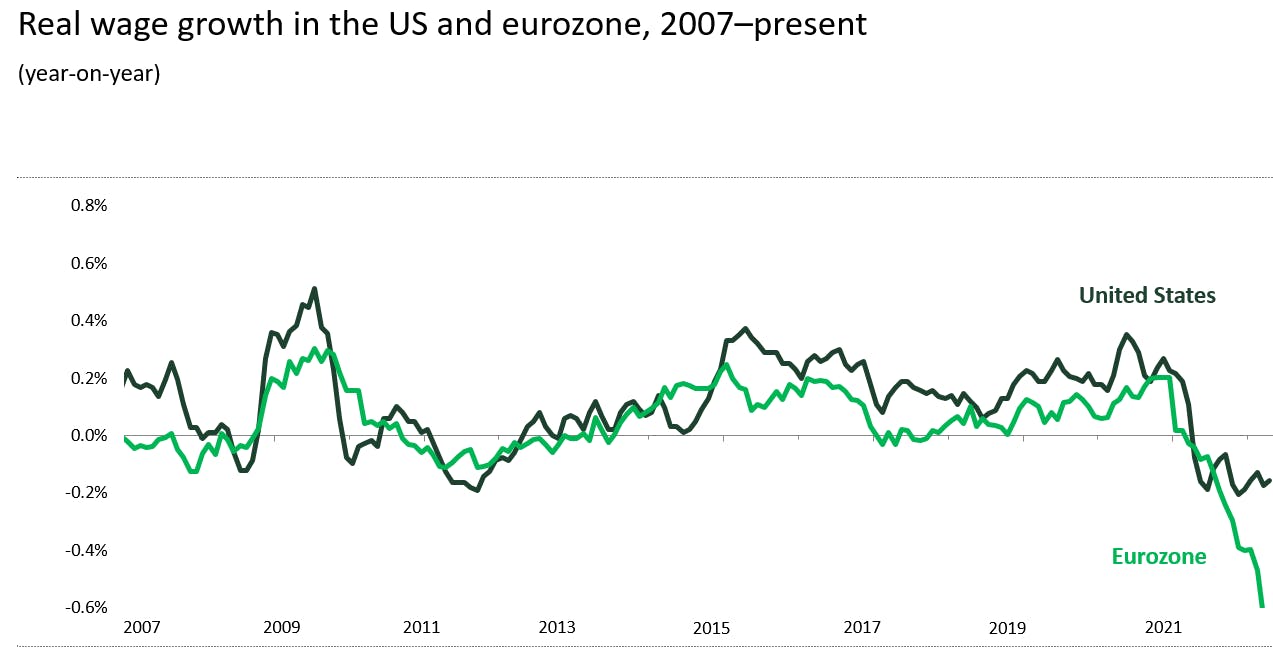

The burden of inflation isn’t the same in the US and Europe

Source: Carmignac, May 2022

In the US, household wealth and excess savings have grown considerably thanks to government measures to help households through the pandemic, coupled with a steep rise in stock markets and home prices. This has put US workers in a strong bargaining position for securing hefty pay rises, with nearly 60% of wage-earners experiencing an increase in their real (i.e. inflation-adjusted) wages. In that part of the world, inflation is being driven just as much by robust consumer spending as it is by the supply shortages resulting from supply-chain bottlenecks.

However in Europe, the jump in inflation is due mainly to higher energy prices along with the supply constraints. Here, real wage growth is deeply negative, putting the brakes on consumer spending. And unless we see a significant adjustment, there’s a strong chance this will lead to a marked slowdown in economic activity.

Rate hikes therefore seem much more justifiable in the US, where a wage-price spiral has taken hold, than in Europe, where most of the consumer-price appreciation is due to outside factors over which the ECB has little control. Given that the ECB must adhere to its mandate and aim for a target inflation rate, we believe it’s now time for European governments to use fiscal policy to address the structural factors of inflation. Fighting inflation too aggressively could end up being counterproductive to economic growth.